As discussed in the Anthony’s 2019 Outlook, political concern persists but economic fundamentals are still strong. The optimist sees opportunity in every challenge, and here we provide some context to support a cautiously optimistic outlook for 2019.

Here are 10 charts providing a case for optimism in 2019:

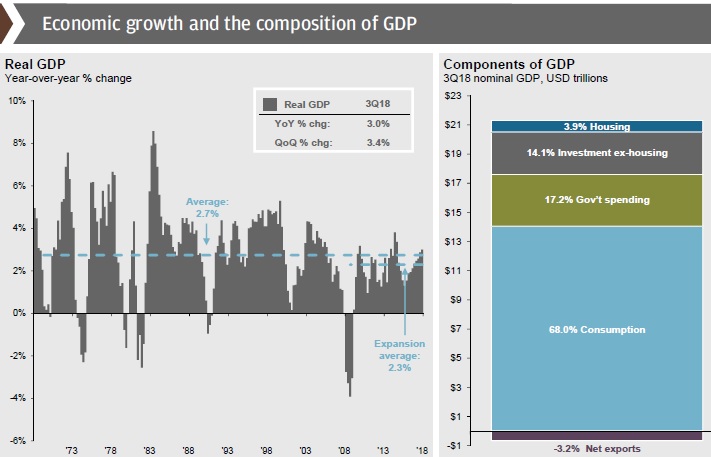

1: The U.S. economy heated up in 2018, but should resume a slow and steady pace in 2019

Growth accelerated in 2018, with real GDP growth reaching 3.0% year-over-year by the third quarter, reflecting a pickup in inventories, government spending, and fiscal stimulus through tax reform. However, 2019 growth is likely to slow without any new tax cuts or stimulus, reverting to the roughly 2% pace that it averaged between 2010 and 2016.

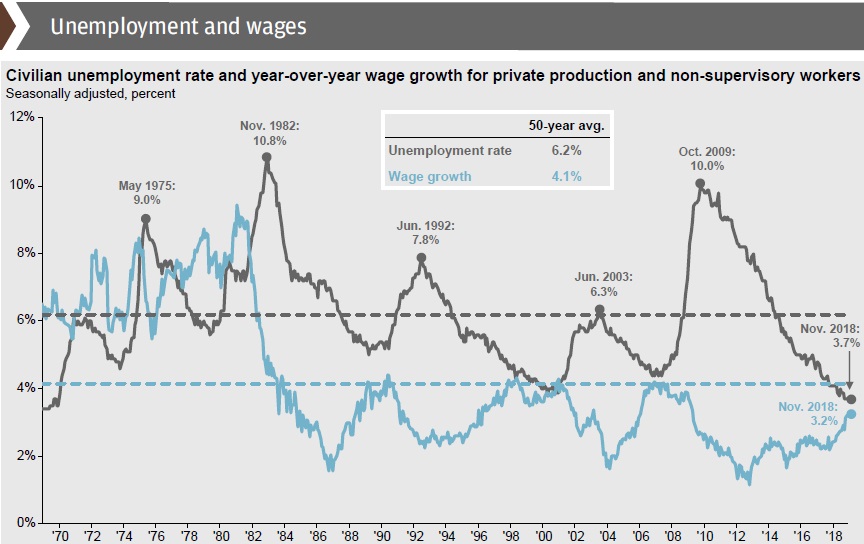

2: Unemployment continues to fall and wage growth has moved modestly

Unemployment has reached a multi-decade low, and factors that limit labour force growth, such as retiring baby boomers and tighter immigration, should continue to push the unemployment rate down. Finally, we have also seen a modest response from wages; however, many companies continue to resist raising wages. Still, difficulty finding qualified workers may force companies to make some concessions, causing wage growth to edge up, but not surge, in 2019.

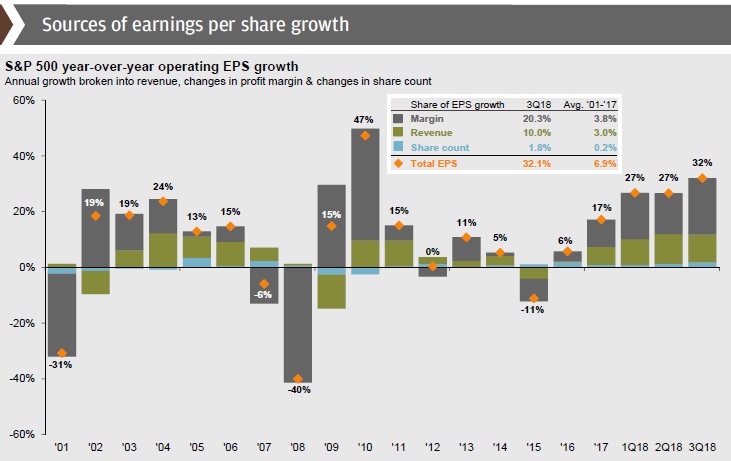

3: Corporate profits have continued to be strong, but will slow

Profit growth was strong in 2018, with the operating earnings per share of S&P 500 companies rising by over 30% year-over-year in the third quarter. Revenues have been boosted by a surge in oil prices and above-trend GDP growth. Margins have also risen thanks to corporate tax cuts and persistently low inflation and interest rates. Share buybacks – a product of excess cash – have also modestly boosted earnings per share.

In 2019 and beyond, however, many of these factors will fade. As a result, earnings growth should return to a mid-single-digit pace. However, the combination of healthy profits and a correction in stock prices have brought equity valuations down to near their long-term averages.

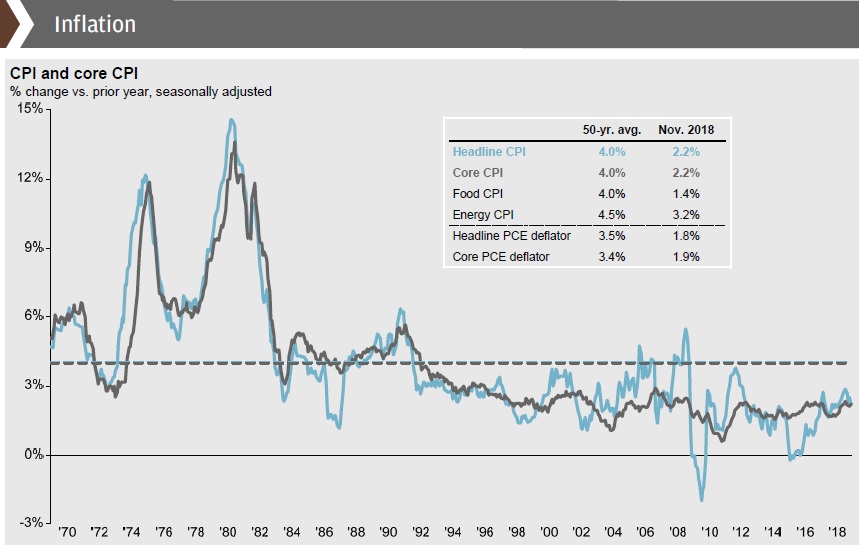

4: Inflation should remain stable

Almost 10 years of monetary stimulus, economic growth, and falling unemployment have succeeded in boosting home prices, bond prices, and stock prices. However, they have not had a meaningful impact on consumer prices. Although oil surged and then retreated in 2018, it should stabilize in 2019, sustaining steady inflation.

Information technology continues to make consumer markets more competitive and this, along with only modest wage growth, suggests that CPI inflation will hover at just over 2% year-over-year over the next 12 months, with inflation as measured by the personal consumption deflator, staying very close to the Federal Reserve’s 2% target.

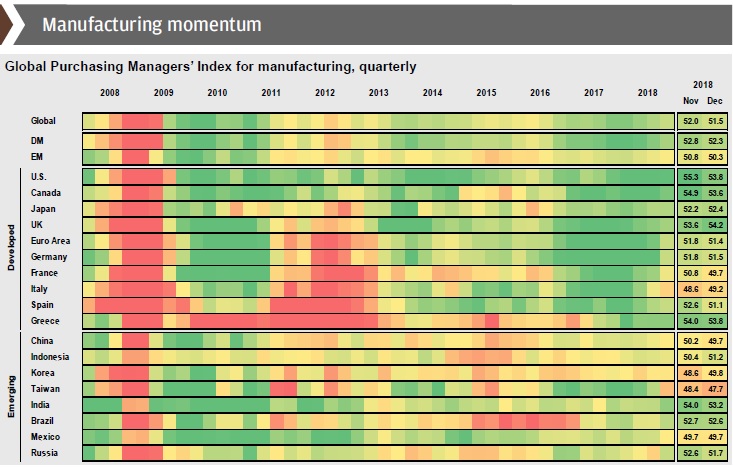

5: The global economy has slowed but remains in expansion mode

After experiencing synchronous global growth coming into 2018, many developed countries lost momentum, and emerging markets faced headwinds from a strong U.S. dollar and tightening U.S. monetary policy. Concerns over trade fed fears of slowing global growth. Nonetheless, PMI data show that most global economies are still in expansion mode, with a few notable exceptions such as Italy, Taiwan and Korea.

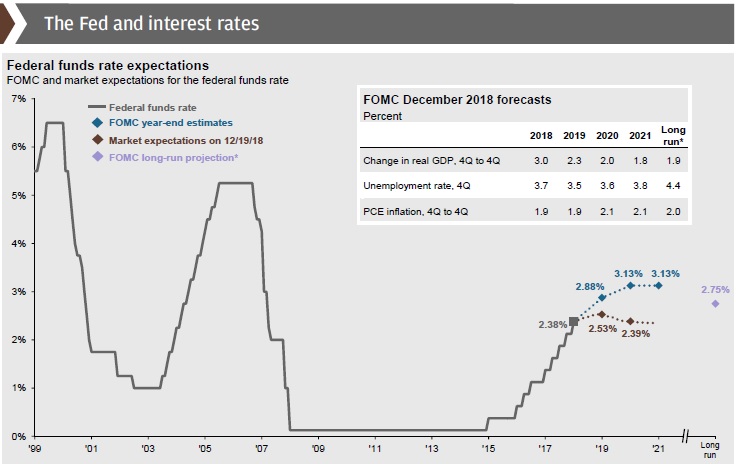

6: The Fed should feel comfortable about raising interest rates

The global economy is generating fewer worries than in recent years and the U.S. is at or near many long-term targets, like unemployment and inflation, making it clear that interest rates are still too low. Moreover, inappropriately expansionary fiscal policy and the desire for future flexibility of monetary policy in the event of a recession has made the need to normalize policy more immediate. Barring any significant negative shocks, the Fed is expected to raise rates by 0.25%, potentially twice in the first half of 2019.

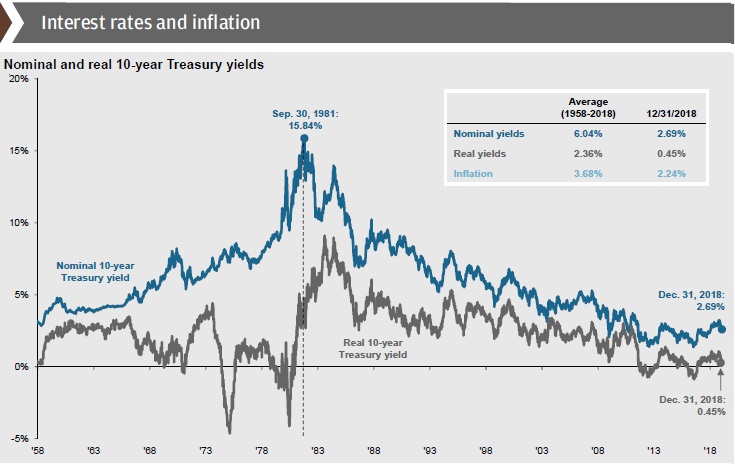

7: Careful fixed income positioning is necessary in a rising interest rate environment

Long-term interest rates remain low, especially compared to historical averages. As the Fed continues to raise interest rates in a low-inflation environment, there is the possibility of a yield curve inversion. While this has historically been a reliable signal of an impending recession, recent unprecedented central bank policy may mean that the yield curve has been distorted. As a result, a yield curve inversion may not mean what it used to.

As rates rise, and the economy continues to grow, credit risk, rather than duration risk, is more appropriate in fixed income investing. That said, as interest rates continue to rise and bonds approach normal valuations, flexibility will become increasingly important.

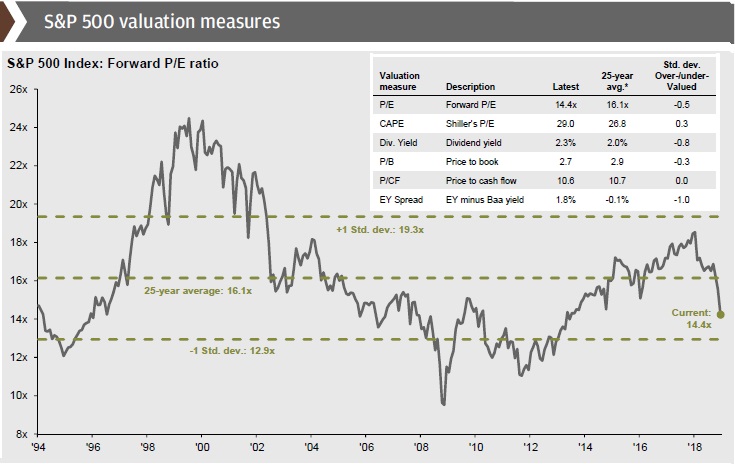

8: U.S. equity valuations are near long-term averages

Market volatility in the fourth quarter of 2018 brought equity valuations closer to their long-run averages, quelling fears that the equity market is overvalued. This was not only due to market corrections, but also to healthy profits. The earnings yield on stocks is still higher than the yield on BAA corporate bonds, making stocks cheap relative to bonds.

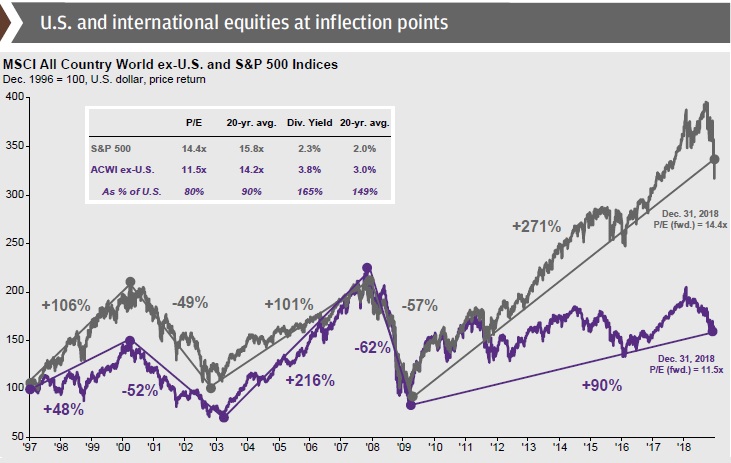

9: International stocks offer long term opportunities

For most of the last three decades, both U.S. and international markets moved sideways. However, come 2011, U.S. markets took off while international markets remained stuck. In 2017, international markets started to outperform, but 2018 was a year of U.S. outperformance, leaving many to wonder if international strength was short-lived. However, international equities remain attractive over the long run thanks to strong economic growth and a downward trajectory for the U.S. dollar. Moreover, valuation measures suggest that international stocks are cheap relative to both the U.S. and their long-term histories.

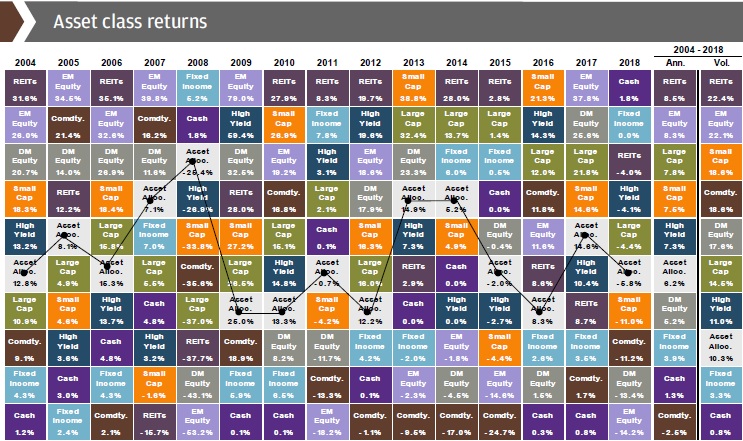

10: Broad diversification and careful portfolio management are required in volatile markets

Despite market volatility at the end of the year and slowing economic growth ahead, equity markets and the economy still have room to run. However, an older expansion and bull market call for a more disciplined approach, with smaller over-weights and under-weights relative to a normal portfolio. It will be even more important for investors to maintain well-diversified portfolios and be willing to adjust as late-cycle risks gradually rise.

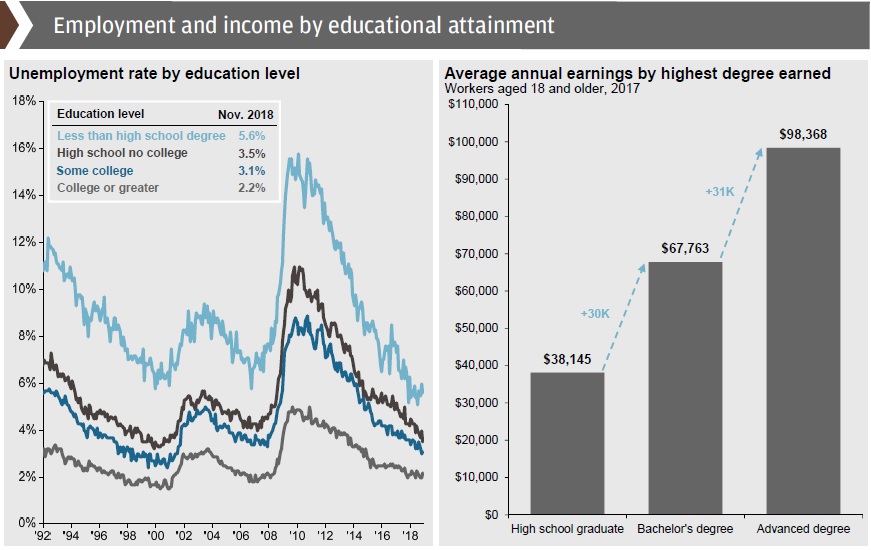

Bonus: Higher education leads to higher income

Don’t forget those RESPs! The higher the educational attainment reached, the higher the average expected annual income.

Remember: the less debt-load a student has as they enter the job market, the better off they are. Avoiding student loan debt in an environment of rising post-secondary tuition requires a greater education savings nest-egg.

Sources: J.P. Morgan, Fidelity Investments

This information is provided for general information purposes only. It does not constitute professional advice. Please contact a professional about your specific needs before taking any action.