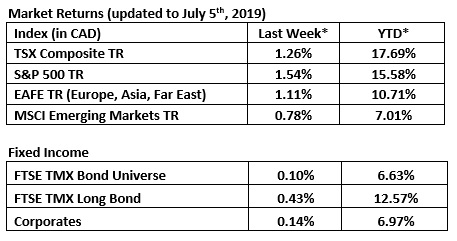

“We really can’t forecast all that well, and yet we pretend that we can, but we really can’t” – Alan Greenspan

2019 Mid-Year Outlook

During this time of year, most investment firms release a mid-year or 3rd quarter market outlook. As usual, some indicators are supportive of a rising market, while others are not. We’ve culled all these outlooks into the following short summary:

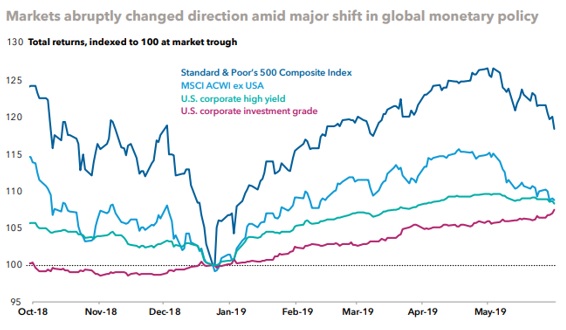

Big Picture – Central Bank Activity: Markets experienced a quick recovery following last fall’s pullback. The U.S. Federal Reserve’s (the Fed) decision to pause rate increases and allow for lower-for-longer rates are extending this economic cycle. Central banks from around the world are either following suit or have resumed/revived stimulus measures.

The market expectations are for the Fed to cut rates by 0.50% to 0.75% by the end of 2019. This will be supportive for both equity and fixed-income markets.

Big Picture – U.S. / China Politics: U.S. President Donald Trump’s tariff increase on Chinese imports in May halted this year’s equity market recovery. While the stock market has since rebounded, the lasting impact can be seen in falling long-term government bond yields, the inverted U.S. yield curve, the slowdown in global trade and weak global manufacturing numbers.

The current consensus on the yield curve inversion is to see if it persists for a few more months before taking it seriously. A combination of Fed easing, China stimulus, and trade compromise could make the recent inversion a false signal.

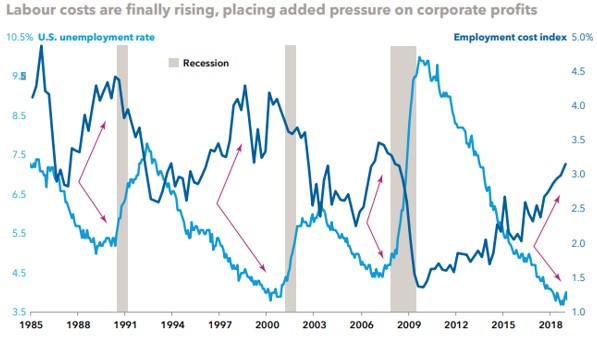

Big Picture – Corporate Profits: Late-cycle conditions are mounting. Rising wages will put pressure on profits, plus a flood of corporate debt could pose problems when the tide turns. Increasing wages inevitably put pressure on profit margins and trigger market volatility.

Europe / Brexit: The ongoing Brexit uncertainty continues to weigh on the British economy. Analysts believe the British Pound Sterling will remain volatile in the short-term, but a rebound in the currency looks likely if the UK’s new Prime Minister can secure a deal with Europe, or if a second referendum is called.

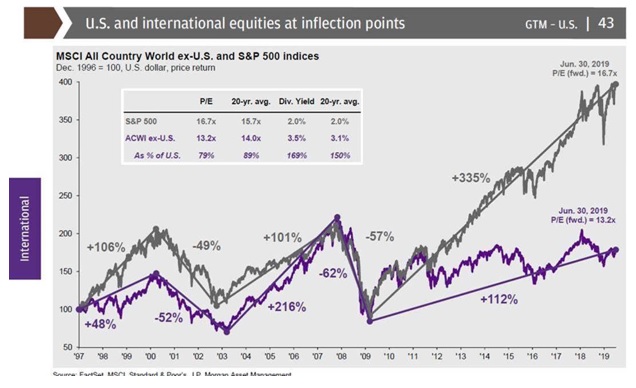

But don’t give up on the UK / Europe. The U.S. has rallied over 300% since the bottom of the 2008 financial crisis. The International space has taken a little longer to catch up. On a relative valuation basis, international markets appear to be trading at a 20% discount to the US market or a 10% discount relative to their historical average:

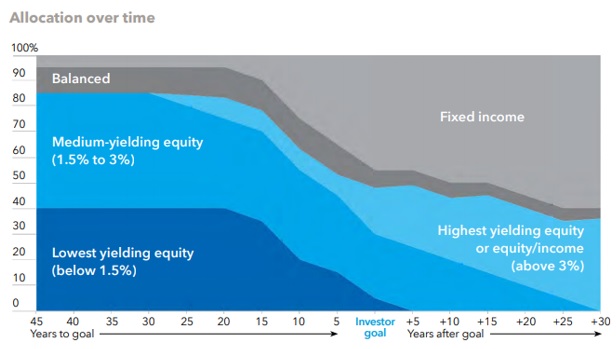

Solution – Update your equity portfolio: Not all equities are equal. For example, a large-cap telecommunications or utility company will have very different risk/reward properties than an up-and-coming technology or mining firm. Different kinds of equities offer a range of characteristics beyond just risk and return. When an investor is in his/her working years, equities can take a more aggressive, growth-orientated approach. As an investor approaches retirement and eventually retires, the characteristics of equities within the portfolio can evolve, taking on a more defensive, equity-income posture. The chart illustrates how equity allocation can be re-characterized over time, in order to pursue investor objective.

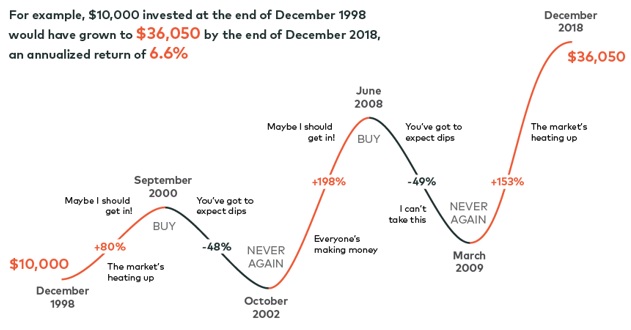

Solution – Keep emotions in check and stay the course: Investor psychology tends to creep in when markets are volatile. A bias of loss aversion can influence investors to want to cash out; however, staying the course over the long term has proven to be the better option, historically.

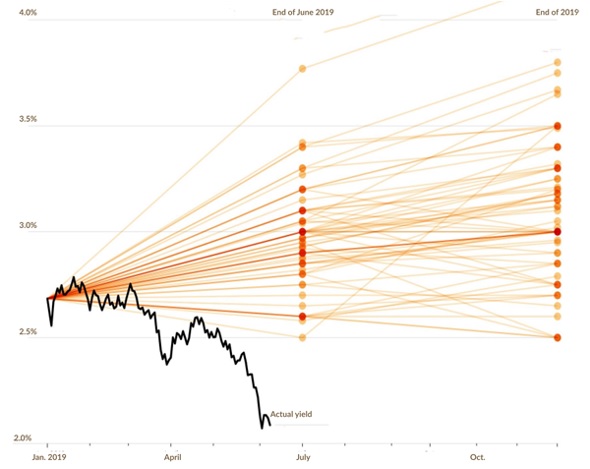

Solution – Ignore the forecasts: There are many credible and educated sources out there, but no one can accurately and consistently predict the future.

At the beginning of 2019, The Wall Street Journal surveyed economists to predict where interest rates would be in June and December of 2019. The graphic below charts these predictions (orange lines) with the actual yield (black line). As you can see, no one came close to predicting the dramatic decline in rates.

We want to keep you informed and educated, but we concede that we don’t know what will happen tomorrow or next year. For this reason, we promote setting a long-term asset allocation, weathering pullbacks and investing in quality companies as being the keys to investment success.

Table: Actual Yield on the 10-year Treasury (black line) Note versus January 2019 analyst predictions (orange lines)

Conclusion: Central bank policy and current valuations suggest equity funds may have room to run, but be ready for a bumpy ride. Investors should expect more late-cycle volatility. It’s not too early to prepare portfolios for rougher seas ahead.

Companies that load up on debt to cover share buybacks and dividends are susceptible to dividend cuts (and stock price declines) when times get tough. In an environment of slowing growth, it makes little sense to invest in feast-or-famine businesses because the feast may be some time away. Higher quality companies are always our preference and we are putting further emphasis on companies with high profitability, returns on invested capital, better balance sheets and better cash generation.

Sources: Capital Group, Dynamic Funds

This information is provided for general information purposes only. It does not constitute professional advice. Please contact a professional about your specific needs before taking any action.