Hello to all You First readers! We hope you are enjoying the sunny weather and the reopening of the city.

We have passed the halfway mark of 2021 and we would like to provide you with a visual update of the major investment themes observed this year.

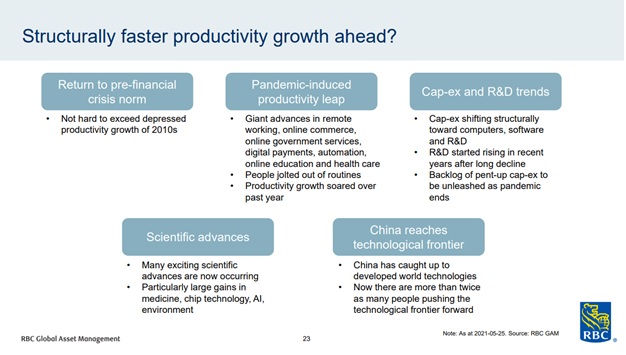

The early phase of the business cycle, marked by impressive post-March 2020 performance, is likely nearing an end. As we enter the next phase, the performance will depend on what lies ahead for inflation, interest rates, and economic growth as well as fiscal and monetary stimulus. We predict a deceleration in these economic drivers, yet our outlook is still positive due to ongoing monetary stimulus.

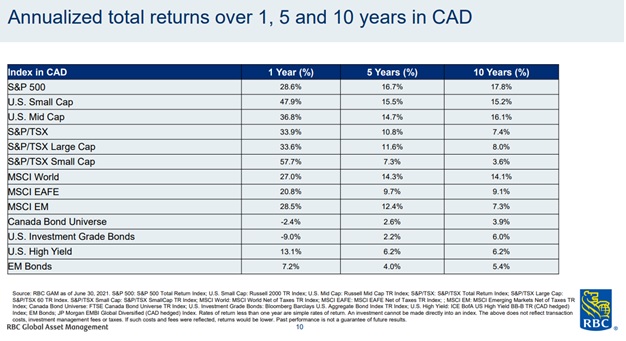

Market Returns: What a difference a year makes! Following a short, but dramatic market drop in Feb-March 2020, markets have rallied ever since. The Canadian market is having the stronger 2021, but the U.S. market has been the main driver of performance for 10 years.

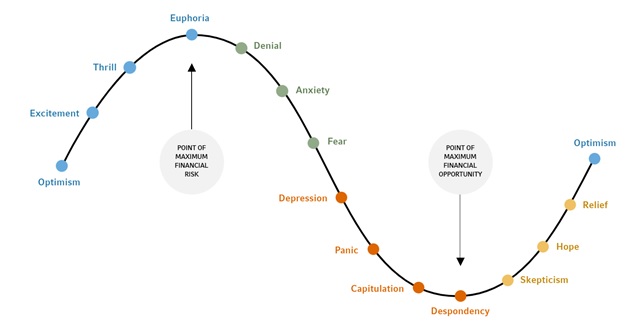

Investor psychology: There are many charts like this, which map the emotions we encounter during a full market cycle. In March 2020, investor sentiment was very pessimistic, and we tried to counter this negativity with historical perspectives on market corrections and recoveries. Today, markets are at record highs and sentiment is at euphoric levels. Against this backdrop, we’ll once again counter all the positivity with the simple reminder that markets do correct from time to time. Sometimes that correction is short-lived (like March 2020), and sometimes it can last years. We’ve seen this before and we will inevitably see it again. This eventuality is factored into portfolio design and retirement planning.

Market timing and diversification: Since the start of 2020, we have seen the following thematic rotations in markets:

- Jan 1 to Feb 15, 2020 – continuation of 2019 rally / 11-year bull run. Broad market appreciation.

- Feb 15 to March 23 – Onset of COVID-19. 40% market correction in 22 trading days. Broad market decline.

- March 25 to April 1 – Governments / central banks around the world announce unprecedented financial stimulus, abruptly ending the market correction

- April to November – “work from home” economy benefits primarily U.S. technology and health care stocks.

- November to June – “reopening rally” benefits discounted value names in the airline, oil, and financial sectors.

- January to June – Inflation concerns benefit cyclical resource stocks (energy, materials) with pricing power. U.S. dollar declines, CAD appreciates. TSX outperforms S&P 500.

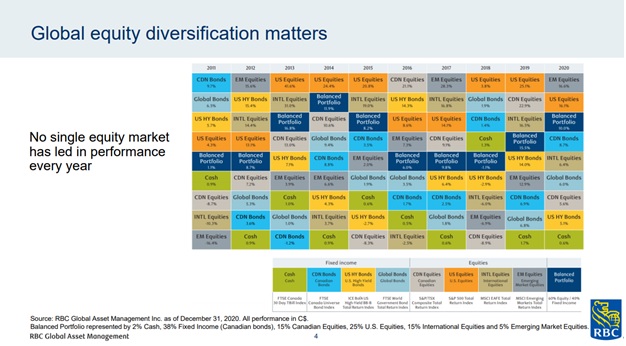

While there is a fundamental reasoning to each of these rallies, it is very difficult to gauge their scope or duration. It is easy to look back, point out, and rationalize a market pattern, but it is impossible to do so in real time. So, what do we do? We allocate your funds across different sectors, markets, and asset classes. We do not expect every portfolio holding to go up in unison all the time. We are less interested in market calls, and more interested in optimized portfolio construction. As you can see in the chart below, a balanced portfolio can capture most of the upside while reducing overall portfolio risk.

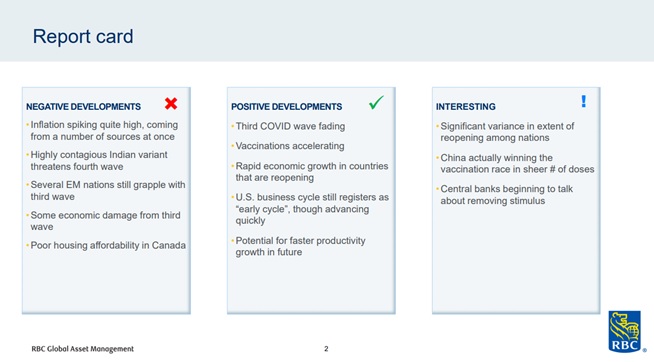

Economic Report Card: It’s always a mixed bag with capital markets. Here are the key factors influencing markets right now, with the positive factors outweighing the negative ones:

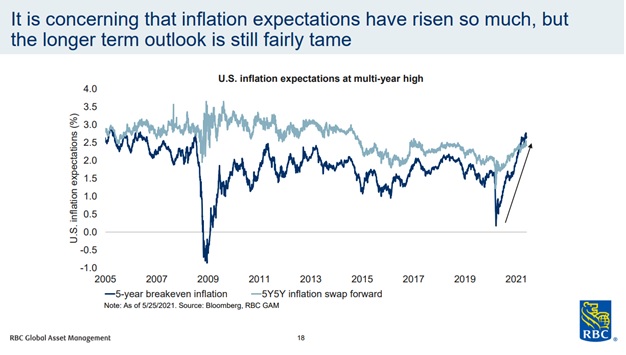

Inflation: The big debate in investment circles is whether inflation is transitory or not. Higher than expected inflation means central banks must increase interest rates and this can cause a short-term shock to markets.

- If inflation is transitory, then it may have already peaked earlier this year. While the Fed may taper, it wouldn’t need to do so aggressively, and rates would not rise until the end of 2022 or 2023.

- If inflation does not keep increasing at the same pace, then it would have to settle back but it would still be higher than the Fed’s 2% inflation target and thus some tapering would be required.

- Should inflation not be transitory then the Fed would need to taper and then tighten more aggressively. However, that would be a risk to market valuations as a higher discount rate implies lower stock valuations.

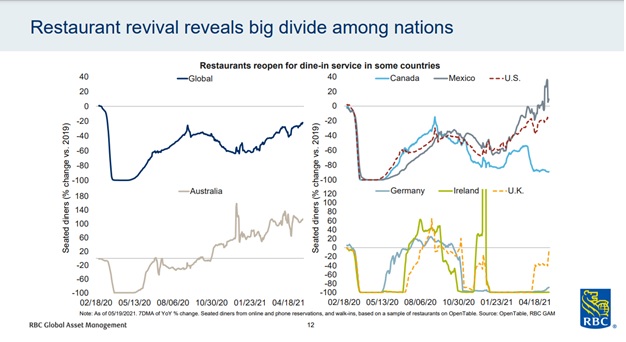

Dining-in at restaurants: We thought this chart was interesting to share. Different countries had very different behaviours when it came to dining-in at restaurants during the pandemic.

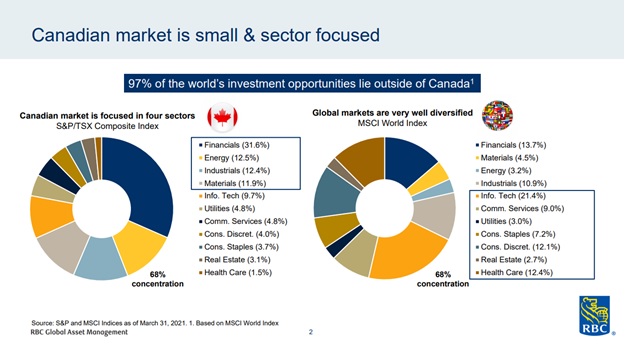

Globally diversified portfolio: Canada and the U.S. complement one another very well in a diversified portfolio. Canadian sectors are largely represented by banks, oil, and natural resources, whereas the U.S. market provides exposure to tech, health care, and consumer goods.

Conclusion: Markets are unpredictable even at the best of times. We’ve seen three different markets in the first six months of the year. We’ve seen a correction in growth stocks because of a spike in rates, a cyclical rally in everything we don’t have enough of (lumber, copper, steel, etc.), and now we are seeing market volatility because of the spike in the Delta variant. Ultimately, we feel most economies and therefore the stock market will be better off over the next twelve months compared to today. We feel the best approach at achieving healthy long-term returns are to hold a globally diversified portfolio of quality equities.

Please contact us with your feedback or questions. Enjoy your summer!

Sources: RBC GAM, Dynamic Funds.