We hope you all had a safe and pleasant summer.

The most common question I have received this year, one that I have asked myself many times, is “how can markets be up amidst the pandemic and economic backdrop?”. On May 29th, we wrote a blog titled “Markets vs. Economy, why markets are only 10-15% off their highs”, which summarized articles by The Globe & Mail and the New York Times on this very issue.

This week, I received a related release from Myles Zyblock, Chief Investment Strategist at Dynamic Funds, which aims to explain the perceived misalignment between the “fair value” of stock prices and current stock prices.

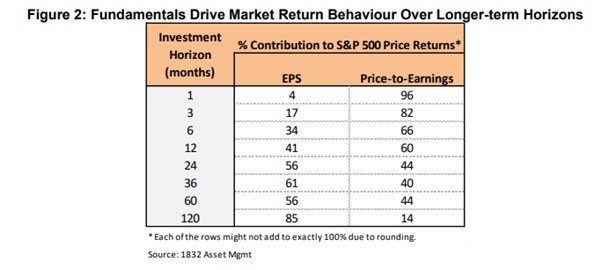

I will try to summarize his article. Markets go up for two reasons: rising earnings (EPS) or price/earnings expansion. The former is a very logical reason based on company fundamentals, but the latter is investor sentiment, a more psychological phenomenon. The table below shows that rising earnings (the fundamental reason), accounts for 41% or less of market performance for time periods under one year:

Thus, when someone asks, “what’s going to happen to markets in the next 3 months?”, a psychologist is apparently better able to answer the question than a financial analyst. Even in a 5-year investment window, “sentiment” still accounts for 44% of market performance. It is not until the 10-year investment horizon mark that fundamental reasons take hold.

I will simply cite Mr. Zyblock for the conclusion:

“So, let’s return to the present day. Stocks have come off the bottom hard since the March low. It sure hasn’t been because earnings were on a tear. It was because P/E multiples expanded; that something has happened to make investors either much more optimistic about future earnings or much more willing to accept equity market risk. Epic policy stimulus is just an educated guess about what that “something” might be. Fiscal policy makers have injected trillions of dollars into the global economy in the form of income support, loan backstops, and tax breaks. Monetary policy makers have driven interest rates into the floor, provided liquidity backstops, and have bought trillions of dollars of bonds in the primary and secondary markets. G4 central bank balance sheets have grown to more than 50% of their GDP, and the promise is to do even more. With this much liquidity hitting the system, is it really any wonder why the stock market’s P/E multiple has responded so positively? A simple “excess liquidity” indicator, measured as money supply growth relative to GDP growth, has exploded upwards. Over time, excess liquidity has shown a strong and reasonably stable positive correlation with stock market valuations. It is hard to see a sustained or significant period of valuation compression when the policy authorities are in full panic mode. As the old Wall Street investment adage goes, ‘markets stop panicking when policy makers start panicking’.”

Please reach out to us with any questions or comments. We wish everyone a healthy and happy fall.

Source: Dynamic Funds